Created by Cc Thum

Property Law course for Real Estate Salesperson in Singapore

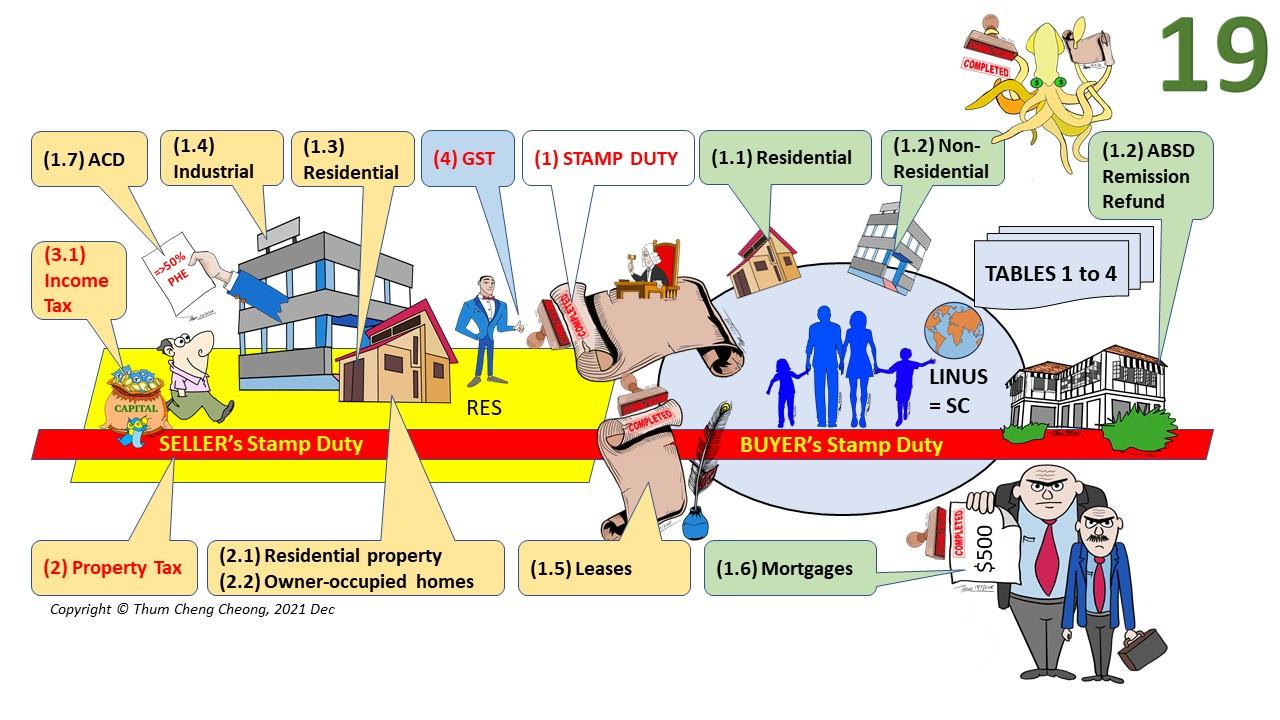

PAYMENT OF SSD.

(i) Before completion.- Conditions Sale 2012,

PAID - Condition 7.4. - Vendor notify purchaser # >=5 clear Business Days before Completion Date # evidence of payment ... certified copy of form of declaration (Commissioner of Stamp Duties) + certificate of stamp duty ( if applicable).

NOT PAID- Condition 7.4.2- Purchaser entitled / not obliged to deduct from purchase price # SSD charged on the Contract # any penalties.- No action against the Purchaser

(4) GOODS & SERVICES TAX (GST) wef 1 April 1994- Goods and Services Tax Act, Sec 8(2)-

"taxable person" registered i.e. RES!- Business with annual turnover >$1 million.- GST on supply of movable furniture and fittings (NOT fixtures).

EXEMPT: sale and lease of "residential properties".

PREMISES: Parties, Property

HABENDUM: (How long) Term, Commencement date

REDDENDUM: Rent, Premium, Deposit

COVENANTS: Rights & Obligations.

(B) INDUSTRIAL PROPERTY bought after 12 Jan 2013.

# 1 year - 15%

# 2 years - 10%

# 3 years - 5%

NOTE:Date of rezoning in Master Plan / change of use to industrial zones / uses = date of acquisition.

(A) RESIDENTIAL PROPERTY:

+ BUYER'S STAMP DUTY (BSD)

# $360K - $1 mil. = 3%-$5.4K

# >$1 mil. = 4%-$15.4K

+ ADDITIONAL BUYER'S STAMP DUTY (ABSD)

NOTE: Refer to (C) below purchases by "Singapore Citizens" (SC).

(B) NON-RESIDENTIAL PROPERTY# 1st $180K = 1%# 2nd $180K = 2%# >$360K = 3%-$5.4K

SSD based on sale price / market price during holding period.

(A) RESIDENTIAL PROPERTY bought

(I) 14 Jan 2011 to 10 Mar 2017.# 1 year - 16%# 2 years - 12%# 3 years - 8%# 4 years - 4%

(II) 11 Mar 2017 onwards.# 1 year - 12%# 2 years - 8%# 3 years - 4%

(1) STAMP DUTY

- Dutiable documents (NOT transactions)

- Immovable property in Singapore i.e. sale & purchase, lease, gift, mortgage

- Stocks and shares

- Stamp Duties Act 1st Schedule

STAMPING TIMELINE from signing/execution

- in Singapore: 14 days

- overseas: 30 days

DELAY: higher of - $10 / duty payable if <= 3 months- $25 / 4 x duty payable if >3 monthsUnstamped documents not admissible as evidence in court

TRUSTEE i.e. purchase property with misappropriated funds from

TRUSTOR (company)

SUBLETTING / SUBLEASE:

Landlord, Tenant + Sub-tenant.

ASSIGNMENT: Transfer interest.

NOVATION: Tripartite agreement replacing contract with new contract same terms between one original party and third party.

Cornet eSS = Construction and Real Estate NETwork e-Submission System

TRUSTEE registered owner

TRUSTOR paid full purchase price

TRUSTOR / DONOR /SETTLOR entrusts property to

TRUSTEE to hold & administer for

BENEFICIARY

Shares

Qualified

Person

(1.7) ADDITIONAL CONVENYANCING DUTIES- wef 11 Mar 2017- ACD on

## sale(seller within 3 years of acquisitions: 12%) and

## purchase (purchaser: 1%-4% residential properties value, 30% on value of assets, 0.2% on share transfer) of residential properties in property-holding entities (PHE) by significant owners (persons / entities) =>50% of the PHE or become one after purchase.

Right of survivorship

(C) ADDITIONAL BUYER'S STAMP DUTY (ABSD)- w.e.f. 12 Jan 2013- on all (wholly / partly) residential properties, all land zoned Residential.

- Excluded: gazetted for compulsory acquisition.

- ABSD is based on purchase price/market value whichever is higher.

- No ABSD for "Singapore Citizens" (SC) purchasing first residential property.

- SC include foreigners under Free Trade Agreements (FTA) i.e. L.I.N.U.S.-

FULL count of properties includes Partial / Joint Ownership.

- TABLE 1 (SC+SC), 2 (SC-SPR), 3 (SC-FR), 4 (SPR-FR)

REMISSION of ABSD- lower ABSD rate / full remission - Co-purchase by MARRIED COUPLE ...SC SPOUSE.-

NOTE: No remission for SPR-FR couple (Table 4).

- Submit an application for remission to IRAS.

- ABSD withheld pending approval.

- BSD must be paid.

REFUND of ABSD

- Married couple ... SC spouse

(i) 2nd property purchase: Paid ABSD

(ii) 1st property sold: within 6 months from date of purchase or TOP/CSC of 2nd residential property.

(iii) 3rd property: No purchases between (i) and (ii).

(3) INCOME TAX on all income- with Singapore source or - received in Singapore even if source in foreign country.

(I) PASSIVE INCOME:- taxable under Income Tax Act Sec 1(f).- rents, royalties, premiumsRENTAL INCOME:(A) Net amount taxable when due and payable (not the date of actual receipt). # Rental income of premises, maintenance, furniture, fittings

DEDUCTIONS: - allowable expenses i.e. property tax. - solely for purpose of producing rental income & - during period of tenancy.

(a) RESIDENTIAL PROPERTIES - wef 1 April 2016: (i) Pre-filled rental expenses (online tax form) of 15% of gross rent of + can claim mortgage interest on loan to purchase tenanted property. Keep documents for 5 years.(ii) claim actual rental expenses incurred with supporting documents kept for 5 years.

(b) TENANTED NON-RESIDENTIAL PROPERTY:only claim actual rental expenses incurred.(B) Jointly owned property- Rental income taxed- Rental loss apportionment. - On all joint owners based on share.(II) GAIN FROM SALE OF PROPERTY

(a) Capital gains are not taxable.

(b) Taxable if trading in properties based on

- frequency

- reasons for acquiring / selling

- financial means ... long term holding period

PROPERTY TAX- on Immovable property- in the Valuation List (VL)- based on Annual Value (AV)

# Gross amount property reasonably expected to be let from year to year.

# Revised whenever market rents change

# May not reflect actual rents

# Reviewed annually.- Property Tax Act Sec 6(1).- "owner" - may or may not be legal owner i.e. person receiving rent, agent, trustee, representative, name in VL.

(1.6) MORTGAGES

- Maximum duty of $500.

- Refer to the Table i.e. 0.4%(LM/VM), 0.2%(EM/T/A).

BUDGET 2013 wef 1 Jan 2014

(1) RESIDENTIAL BUILDINGS

(a) unoccupied despite reasonable efforts to find a tenant. # Non-owner-occupied residential bldgs property tax rate.

(b) undergoing repairs/building works intended for owner-occupation. Condition: owner-occupied =>1 year after completion of repairs / works. #Owner-occupied tax rates for duration of repairs / works up to max 2 years.

(2) NON-RESIDENTIAL BUILDINGS(a) undergoing repairs to render fit for occupation or vacant despite reasonable efforts to find a tenant # Property tax rate of 10% for non-residential buildings.

(3) VACANT LAND (a) Undergoing housing development Intended for owner-occupation Condition: owner-occupied => 1 year after completion of house. $$ Owner-occupier tax rates for residential buildings for the duration of housing development up to max 2 years.(b) Other vacant land $$ 10% during development period.

(1.5) LEASES- Based on Average Annual Rent (AAR)

- AAR: Higher of the

# Average annual contractual rent

# Annualised market rent Includes payments for furniture & fittings, maintenance fee, conservancy charges where applicable.

(i) Leases <= 4 years- Higher of total contractual / market rent

(ii) Leases > 4 years- 4 times AAR

NOTE: Refer to Tables for documents executed(a) before 22 Feb 2014(b) on or after 22 Feb 2014.

PROGRESSIVE TAX RATES wef 1 Jan 2015(2.1) RESIDENTIAL PROPERTY (exclude residential land)- refer to table.

(2.2) OWNER-OCCUPIED HOMES- refer to table for concessionary tax rates- applied to one home owned and occupied- only current owners can apply

Not qualified: - company, association,..

Not applicable to non-residential properties/land